Investing in a holiday rental? Congrats—you’re now the proud owner of a financial commitment that deserves more than just a simple high-five and a holiday insurance policy. Why? Because holiday insurance … yeah, it’s not going to cut it for the wild ride that is short-term rentals.

Here’s the deal—at Ridgewaters Kiama, we get it. Property damage, guests deciding your staircase is their personal adventure park, and the ever-looming regulatory hydra … all chomping away at your returns. The solution? Smart protection strategies. They aren’t just optional; they’re essential—to keep your property and that sweet income stream safe and sound.

What Insurance Do You Actually Need?

Standard homeowners insurance is like a Swiss cheese parachute for your holiday rental investment-full of holes. Period. In 2023, the Australian Financial Complaints Authority got bombarded with 1,847 insurance disputes over short-term rentals, mainly thanks to these coverage gaps. Your garden-variety policy gives the boot to commercial activities, leaving you high and dry when guests trash the place or take a spill.

Short-Term Rental Insurance Essentials

So, what’s the play? Specialised holiday rental insurance-yep, it’s gonna cost you 15-25% more than your standard stuff, but here’s the thing: it’s got your back for commercial use, guest injuries, and property damage during rentals. QBE and Allianz, those big dogs, have you covered with short-term rental products that include public liability up to a cool $20 million and contents coverage for your fully decked-out pad. You’re shielded from guest theft, accidental damage, and those lovely acts of malice your regular policy wants no part of.

Liability Protection Requirements

Public liability insurance isn’t just a nice-to-have- it’s a must when random folks crash at your place. Picture this: someone slips on wet tiles and boom, you’re staring down claims that blow past $500,000 (thumbs up to the Insurance Council of Australia for those figures). The minute you take money from guests, standard homeowners policies pull the Houdini act on coverage, creating massive exposure gaps for holiday rental owners.

Contents Coverage Calculations

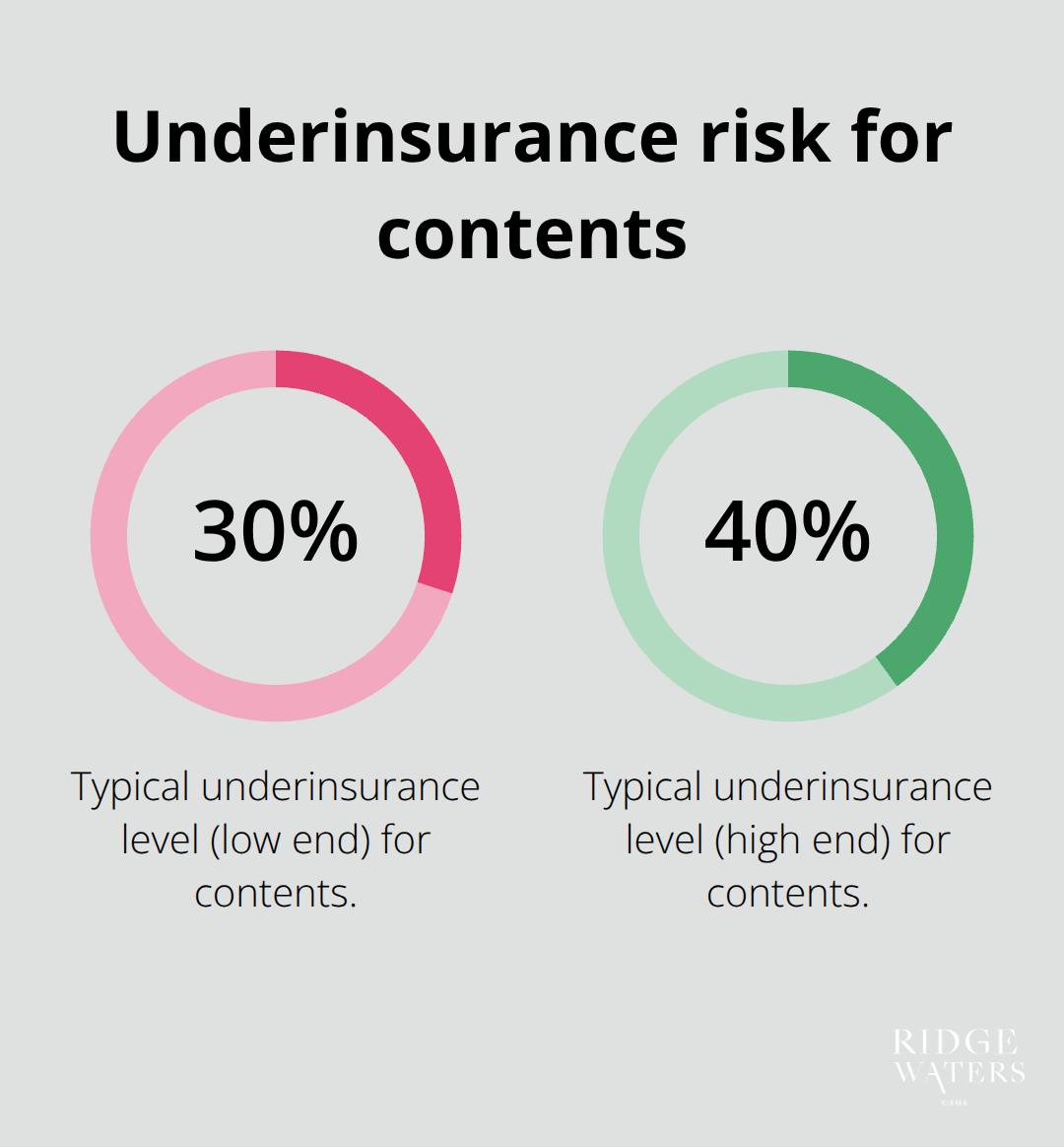

Let’s talk contents insurance-this needs to reflect the true replacement value of all your stuff-furniture, electronics, appliances, you name it, at today’s prices. A lot of folks skimp here, underinsuring by 30-40%, and it comes back to bite them when they have to fork out for a new fridge or designer couch. Do the math on your contents value annually and tweak your coverage to dodge those nasty out-of-pocket surprises.

And hey, beyond just insurance, your holiday rental’s got its own labyrinth of regulatory and compliance hoops to jump through, which can hit your investment returns if you don’t play by the rules.

What Legal Hoops Must You Jump Through?

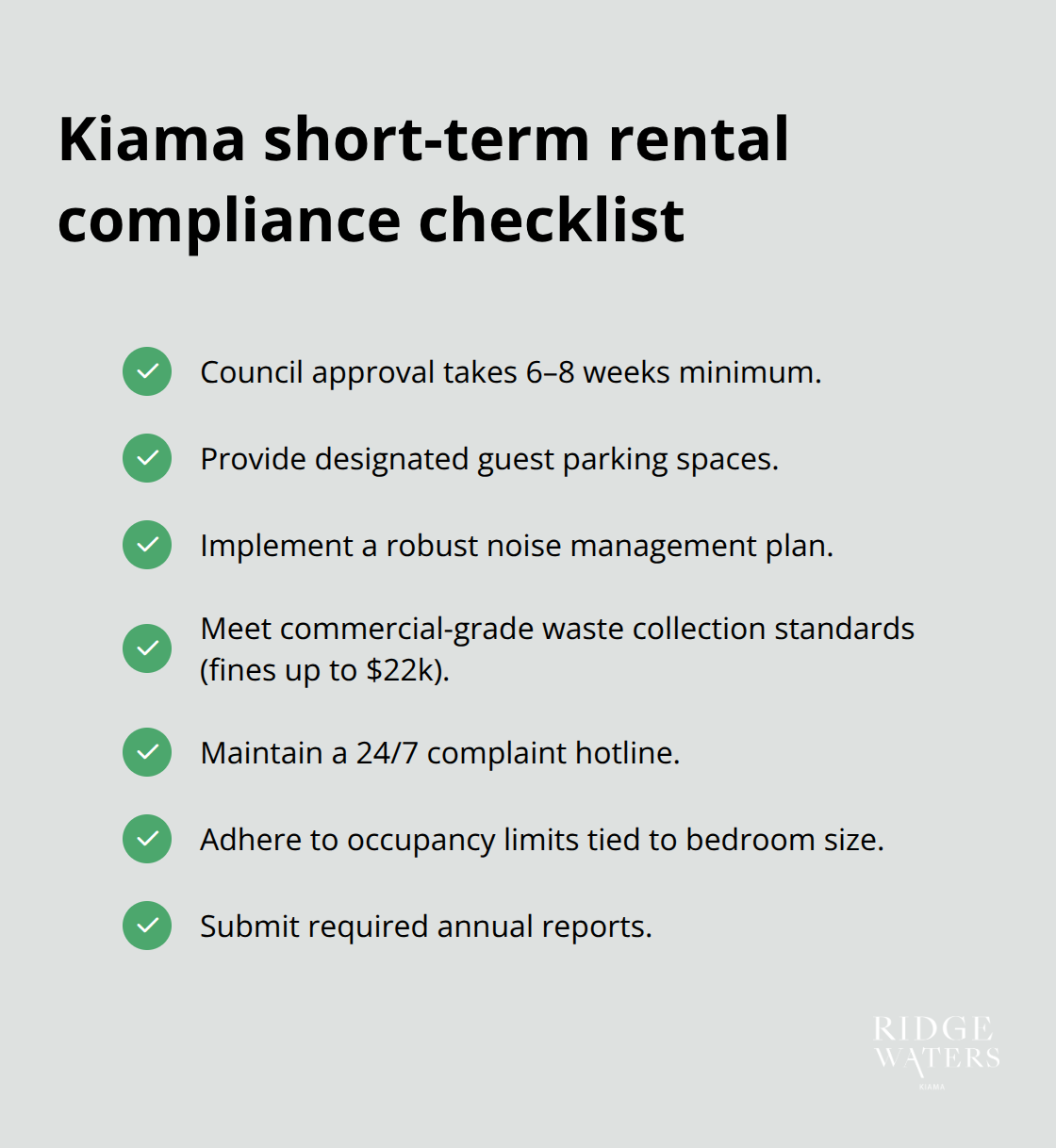

So, you’re thinking about diving into the wonderful world of short-term rentals in Kiama? Well, gird your loins because there’s a gauntlet of red tape. Step one: you need the council’s blessing-6-8 weeks minimum, folks. And it’s not just any kind of blessing; we’re talking about a laundry list a mile long-parking spaces (yeah, actual designated ones), and a noise management plan that Houdini himself couldn’t slip past. And let’s not forget waste collection-if you don’t meet those commercial-grade standards, then talk to the hand-fines go up to $22k. Parking for guests? Non-negotiable.

Round-the-clock complaint hotline? Mandatory. Oh, and don’t even think about packing that place like a clown car-occupancy limits are tied to bedroom square footage. Annual report card time!

Guest Verification and Platform Compliance

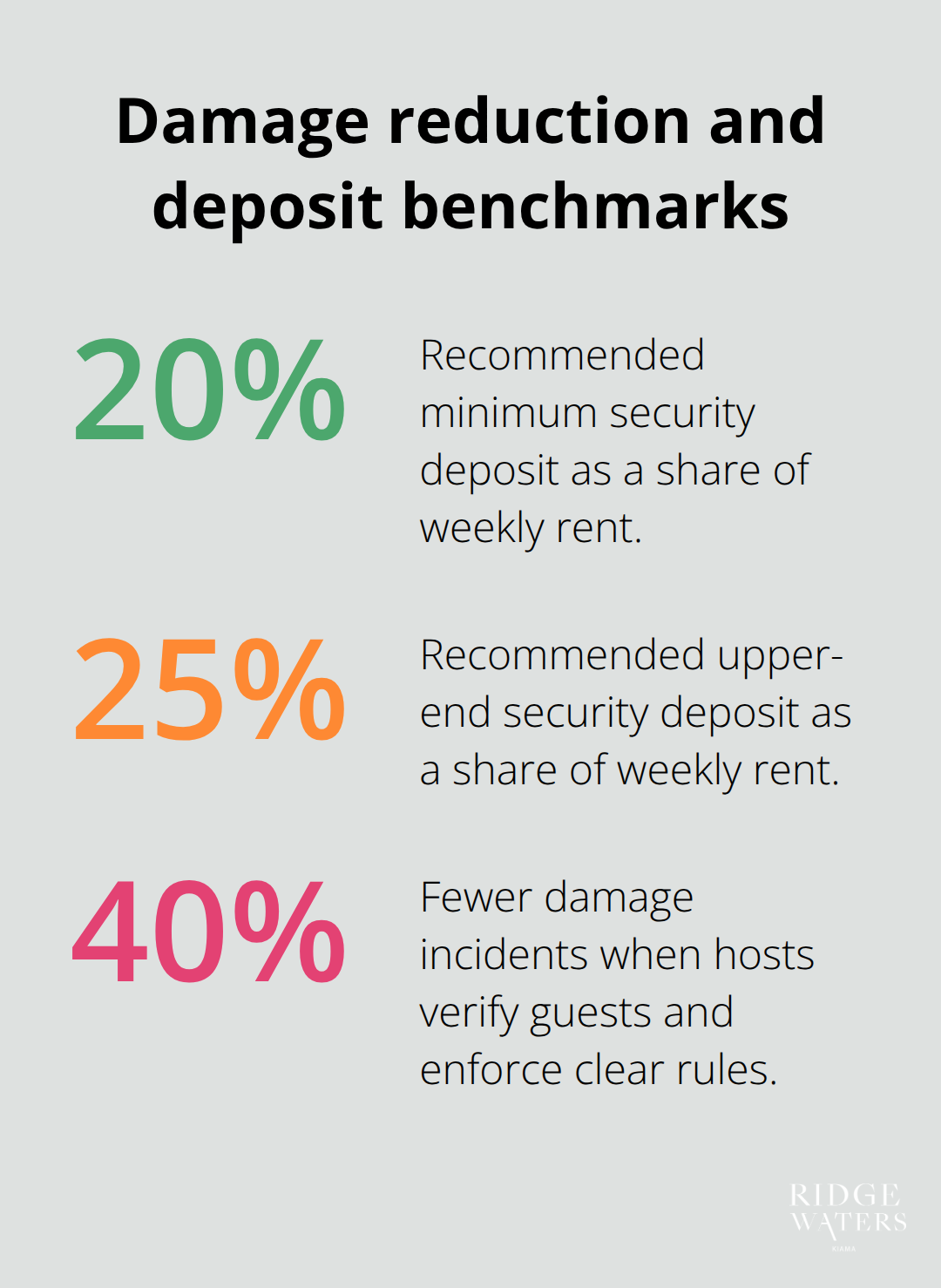

Airbnb and Booking.com-yeah, they want you to verify guest identities, but here’s the pro tip: get chatty. Vet these folks like you’re hiring a live-in nanny-not just some thumbs-up curtain-twitcher. Dive into reviews, line up security deposits like dominoes. Data shows that eagle-eyed operators report 40% fewer damage debacles. Set house rules that are so clear, they might as well be tattooed on your forehead-parties, smoking, pets… all a hard pass. Everything goes through platform messages-that’s your paper trail defence line if guests go rogue. Tech up with smart locks-no keys, no fuss, less stress.

Emergency Preparedness Standards

Safety first, with a twist-NSW mandates photoelectric smoke alarms because AS 3786:2014 isn’t just a catchy code, it’s law. Throw in fire extinguishers, first aid kits, and phone numbers in bold (and visible) for emergency heroes. Detail those exit strategies like a heist movie-maps by every door. And if your place is rocking gas appliances or a pool? Carbon monoxide detectors and pool barricades-they’re on you. Keep emergency contacts conspicuously visible-pop them by the fridge, by the exits, wherever. Frequent checks of your safety gear could save you a bundle in lawsuit dodgeball.

Noise and Neighbour Relations

The noise police of Kiama are out there, and they mean business-10 PM to 7 AM, zip it up. Invest in noise monitors-they won’t rat you out with real conversations but will ring the alarm on decibels. Guests need crystal clear noise don’ts and a hotline for 24/7 peace-disturbance intervention. Too many noise strikes? Kiss that permit goodbye. Keep neighbours on side-make like Switzerland-neutral, proactive, and quick on the draw when issues crop up.

Staying on the right side of law and order shields your investment, but sprinkling in some financial insurances? That’s the secret sauce for holiday rental mastery.

How Do You Protect Your Rental Income?

Security Deposits and Damage Protection

Security deposits-you’d think it’s simple, right? But nope, most hosts totally whiff this part, setting amounts that feel more like a dart throw. So, here’s the deal: set yours at 20-25% of the weekly rental rate. Not just pulling $500 out of thin air.

Australian Consumer Law is the ruler of the damage protection kingdom, so go paparazzi crazy with photos and receipts. The savvy hosts? They’ve got platform-held deposits AND a separate damage bond-a double whammy courtesy of services like Superhog, handling up to $3,000 in damages without having a guest throw a tantrum.

Revenue Loss Insurance Coverage

Revenue protection insurance isn’t just a good idea anymore-it’s the law (okay, not literally…). COVID gave us a crash course in how fast bookings can turn into vapour. Zurich and QBE are now rolling out the red carpet with holiday rental income protection, covering you for 12-18 months when disaster strikes, be it repairs or some regulator throwing a wrench in your plans. You’re looking at a premium of 2-4% of your annual rental income. Seems steep? Well, one pipe decides to go Niagara Falls in your pad, and suddenly, that premium looks like a steal.

Tax Deduction Strategies

Enter the Wild West of tax strategy. This is where you separate the savvy operators from the weekend warriors. Depreciation’s like magic-it can offset 15-20% of your property value over 25 years using the Australian Taxation Office building allowance schedule. The golden rule: claim everything. We’re talking cleaning supplies, management fees, insurance, repairs, even that shiny new coffee machine for guests’ caffeine fixes. Interest on investment loans? Still fully deductible (unlike when you’re living in your own fortress).

Occupancy Rate Requirements

So, occupancy rates-treat them like sacred texts. The ATO’s watching, differentiating between legit rental operations and your personal holiday hideaway. Fall short of 140 days rented annually, and-boom-tighter deduction limits hit you. The solution? Professional property management fees. Sure, they average 15-25%, but they’re immediate tax deductions and could fatten up your rental income with killer marketing and guest-screening skills you thought only unicorns possessed.

Final Thoughts

Your investment at Ridgewaters Kiama-yes, that slice of paradise-needs one serious layer of protection… much more than your everyday holiday insurance plans. We’ve walked you through how specialised short-term rental insurance, rigorous legal compliance, and smart financial strategies are the secret sauce to safeguarding your returns in Kiama’s cutthroat market. Those who double down with a full-on protection framework report 40% fewer damage incidents and snag better occupancy rates.

So, what’s your investment safety net? Three non-negotiables: insurance coverage that doesn’t flinch-public liability up to $20 million, thank you very much, ticking every box on Kiama Council regulations, and solidifying financial protections with security deposits plus revenue loss coverage. First steps? Level up your insurance policy, grab the necessary permits, and nail down foolproof guest verification procedures. Security deposits? Aim for 20-25% of your weekly rates, lock in the required safety gear, and keep meticulous records for tax deductions (we’re talking 15-20% off your property value annually).

Here at Ridgewaters Kiama, we offer luxury apartments that are the ultimate springboard for shored-up holiday rental investments. With striking modern design and a prime coastal location just a stone’s throw-90 minutes-from Sydney, we attract top-notch guests while equipping you with the security features savvy investors demand. These properties blend high-end amenities with the strategic benefits that serious holiday rental investors are chasing in today’s buzzing market.