Owing an apartment at Ridgewaters Kiama is an exciting investment—coastal views, capital upside, bragging rights. But don’t kid yourself: the mortgage is just the opening act. Body corporate fees, maintenance levies, insurance gaps and surprise repairs… those are the encore that can hollow out your savings. If you’re not primed, they’ll show up uninvited and expensive—fast.

This guide is your damage-control playbook—hidden costs spelled out, budgeting tactics that actually work, and protection options (rental insurance, mainly) that transfer risk instead of burying it in hope. We’ll walk you through building financial resilience, triaging repairs, and fortifying your coastal property so a busted pipe doesn’t become a financial catastrophe.

The Real Price of Owing at Ridgewaters Kiama

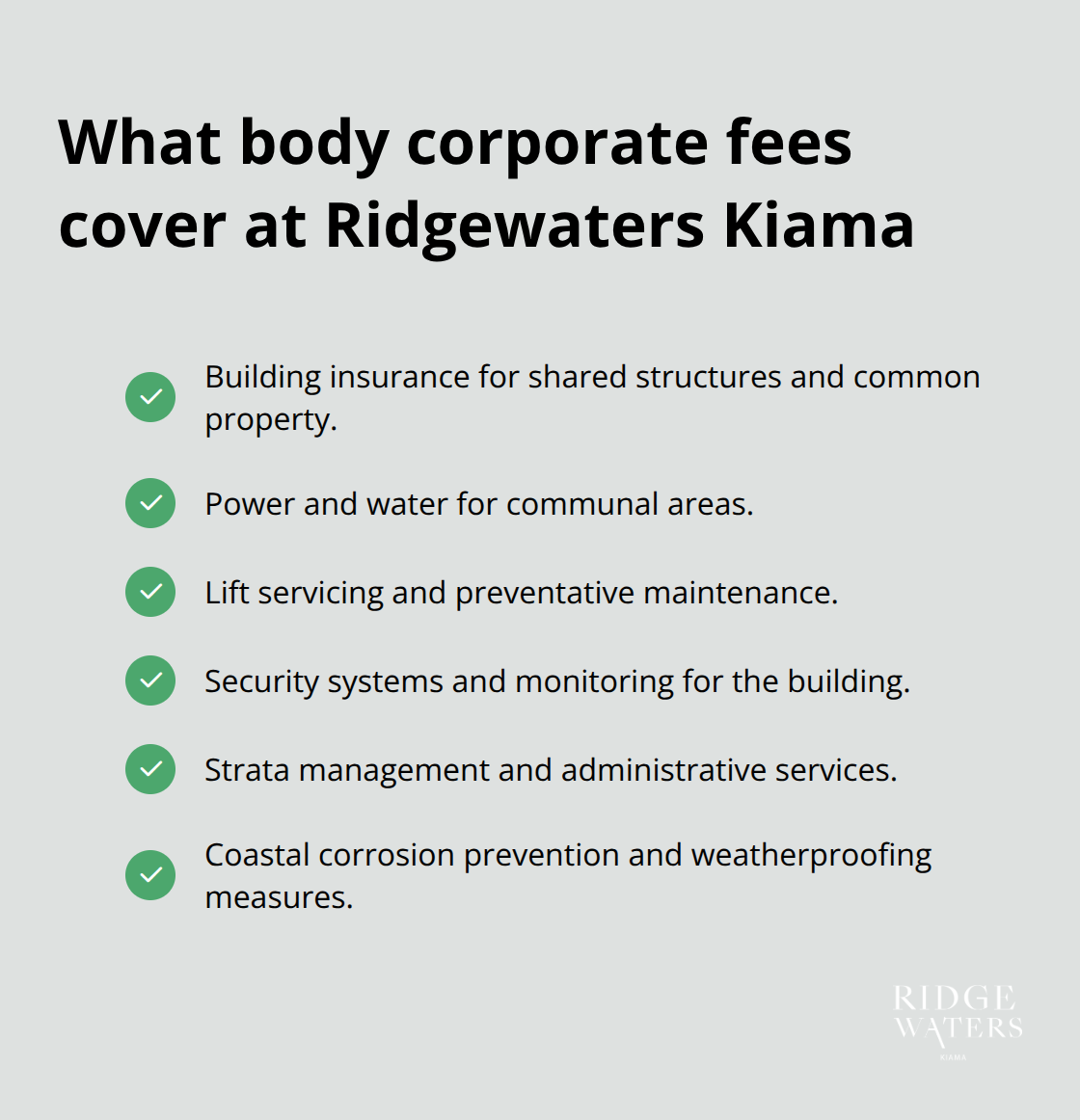

Body Corporate Fees and What They Cover

Body corporate fees at Ridgewaters Kiama aren’t optional-they’re the toll you pay to live in a shared building without chaos. Think shared infrastructure, common-area upkeep, and basic building management. What do you actually get for your money? Building insurance, power and water for communal spaces, lift servicing, security systems, and strata management.

Coastal living adds an extra line item-salt-air corrosion prevention, weatherproofing, more frequent inspections of external elements. Expect fees to creep up each year; coastal complexes commonly see 3–5% increases driven by inflation, ageing systems, and stricter building codes. Boring, inevitable, and expensive.

Then there are the surprise bills-special levies that drop like anvils. A failed roof membrane, botched waterproofing, or a dying lift can trigger one-off charges of thousands. Don’t buy blind: request the last three years of meeting minutes and financial statements. Look for deferred maintenance, planned capital works, and any flagged structural concerns. No building condition report in five years? Big red flag-walk in with caution (or a really fat contingency fund).

Property Management and Insurance Gaps

If the body corporate outsourced admin, expect property management fees-usually 5–10% of total body corporate revenue. That pays for accounting, tenant liaison, compliance-essentially the stuff that keeps the building from becoming a soap opera. Some complexes roll this into the base fee; others tack it on separately. Read the fine print (yes, all of it).

Insurance is where people trip up. Building insurance covers the structure-not your stuff, not your liability. The body corporate’s policy covers fire, storm, and structural damage but typically excludes theft from your unit, water damage from a busted pipe inside your apartment, or liability if someone tweaks an ankle in your place. Short-term rentals make this messier-many owners at Ridgewaters Kiama who list on Airbnb discover their standard home and contents insurance explicitly excludes income-generating activities. Guest slips in the shower? Property trashed by a party? Insurance might say “nope.”

Income protection for short-term rentals runs AU$400–AU$800 a year and covers lost rental income if the place is uninhabitable. At a coastal property-where storms and emergency repairs can bench your revenue for weeks-this isn’t optional if you rely on rent.

Repair Costs and Appliance Warranties

Surprise repairs are the stealth tax of ownership-they show up at 2 a.m. on a Sunday and drain your account. Plumbing failures, electrical faults, appliance meltdowns, water intrusion-they don’t negotiate. Replace a hot water system at a coastal apartment and you’re looking at AU$1,200–AU$2,000; a corroded AC unit? AU$1,500–AU$3,000.

Appliance warranty plans exist for a reason. In Australia, basic coverage runs AU$500–AU$1,000 a year with service-call fees around AU$60–AU$100. The math is simple: a washing machine motor at AU$350–AU$500, an oven control board at AU$400–AU$700-these costs justify warranties fast. But warranties have teeth-they exclude pre-existing issues, poor maintenance, and cosmetic damage. Before you sign, confirm the plan actually covers your appliances and that the warranty provider services Kiama.

Building Your Financial Defences

Don’t mix your emergency cash with maintenance money-set up a dedicated maintenance reserve. Split your planning into regular maintenance, cyclical replacements, and unexpected repairs. That framework helps you allocate dollars rationally instead of panicking when the next levy arrives.

Track what breaks. Ask the seller about historical maintenance costs and recurring headaches. Neighbours will tell you the truth-more than glossy sales brochures ever will. Demand service records for major systems: roof, external cladding, plumbing risers, electrical infrastructure. Coastal builds age faster-salt and moisture accelerate decay-so a five-year-old building in Kiama can need more love than a ten-year-old inland equivalent. Financial planning has to account for that accelerated wear cycle and the higher frequency of repairs that comes with life by the sea.

How to Budget for Coastal Property Ownership

Understanding Your True Annual Costs

Your mortgage payment? That’s the appetizer. The real meal starts after settlement – especially at Ridgewaters Kiama. The Australian Bureau of Statistics says home ownership costs have jumped roughly AU$100,000 over the past four years… and coastal homes wear out faster than inland cousins. Salt air, moisture, storm exposure – they’re not subtle. Your maintenance budget needs teeth from day one. Most apartment owners learn this the painful way: special levies creep up 3–5% a year, surprise repairs wreck savings they never set aside. The solution isn’t rocket science – it’s discipline and cold, hard numbers.

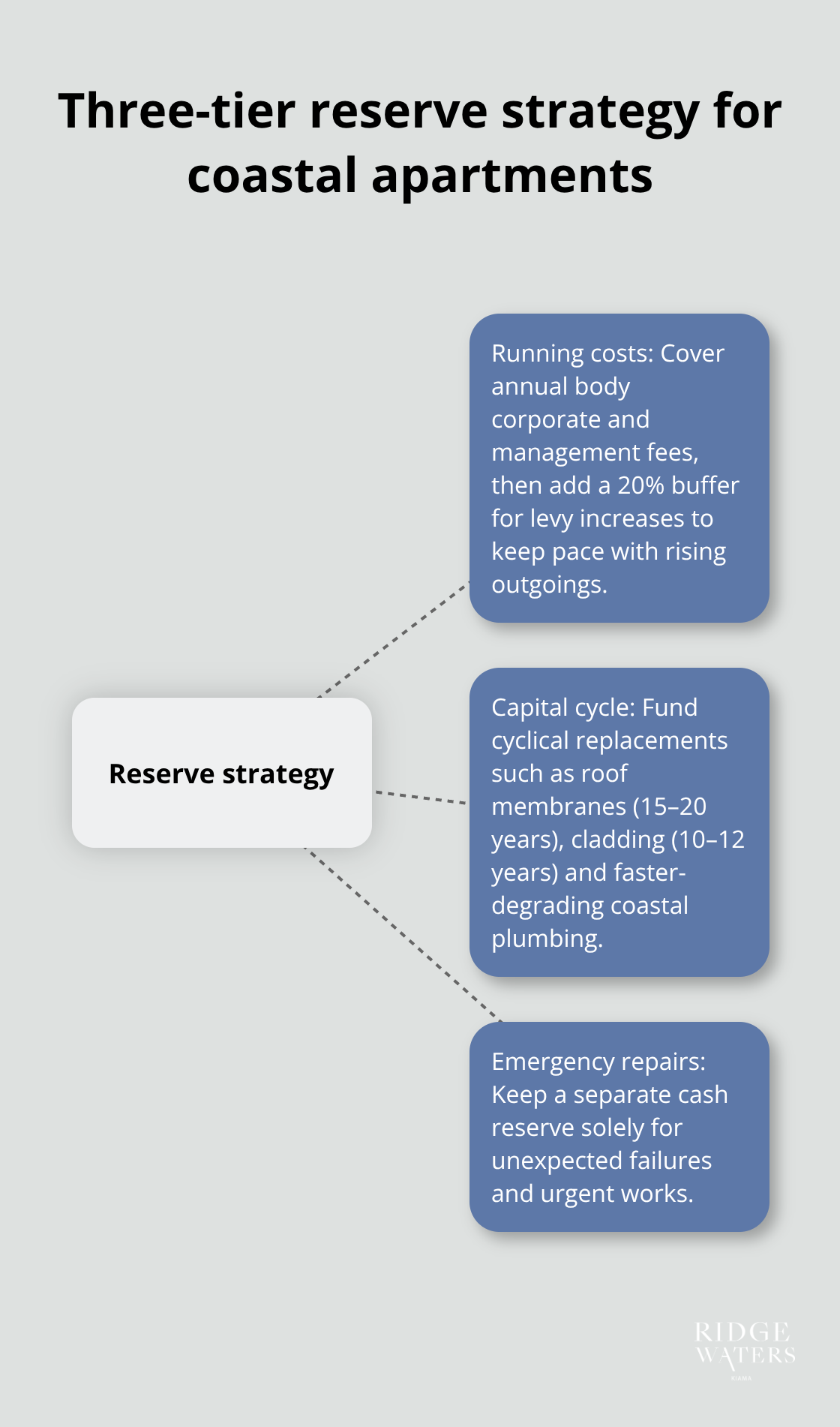

Start with a three-tier reserve strategy. First – add up your annual body corporate fees and property management costs (typically 5–10% of body corporate revenue), then tack on a 20% buffer for the inevitable levy hike. Second – stash capital expenditure reserves for cyclical replacements: expect roof membranes to fail around 15–20 years, external cladding to need attention every 10–12 years, and plumbing to degrade faster on the coast. Third – build an emergency repair fund that’s separate from both of the above.

Applying the 1–4% Rule to Coastal Apartments

The 1–4% rule actually holds up for coastal places. If the building is under 10 years old, budget 1–2% of your apartment’s value each year for maintenance; older coastal stock? That jumps to 3–4%. So an AU$800,000 apartment equals AU$8,000–AU$16,000 a year in reserves. Make it monthly – that way a repair bill doesn’t ambush your cash flow.

Airtasker pricing (June 2025) shows typical apartment maintenance jobs run AU$4,900–AU$12,000, median near AU$9,200 – so your annual reserve should cover a major job plus routine upkeep. Do your homework before you sign: demand five years of meeting minutes and maintenance records. Neighbours are priceless – they’ll point out recurring failures (rotting balconies, failed waterproofing, corroded pipes) the sales pitch glosses over. Coastal properties deteriorate faster than inland equivalents – so a five-year-old Kiama building might need more aggressive capital planning than a decade-old inland development. Don’t assume age equals safety.

Coastal properties deteriorate faster than inland equivalents

Navigating Market Fluctuations and Climate Risk

Coastal markets slam harder on the way down and sprint faster on the way up – driven by interest rates, tourism, and climate headlines. Kiama – 90 minutes south of Sydney – pulls double duty (residential plus holiday rentals), which means your asset is exposed to two demand cycles. Interest rate rises typically shave 8–12% off values in established coastal markets before things settle. If you’re banking on income from short-term lets, watch occupancy and nightly rates quarterly – a 10% drop in bookings is not a gentle nudge, it’s a warning siren.

Then there’s climate risk – flood and bushfire premiums bite both appreciation and insurance costs. Check council flood maps and bushfire assessments before you commit. Insurers will price that risk into your premiums, so factor it into annual outgoings. Market timing matters if you plan to exit within 10 years; if you’re a long-term resident or retiree, cash flow and manageable maintenance trump price swings. Either way – lock in your reserves now. They’re not optional; they’re your hedge against surprise repairs and market downdrafts that can force a fire sale.

With reserves in place and the market reality accepted, the next step is picking the right insurance to shield your investment from the specific risks coastal ownership brings.

What Insurance Actually Protects Your Coastal Apartment Investment

Building Insurance Covers the Structure, Not Your Belongings

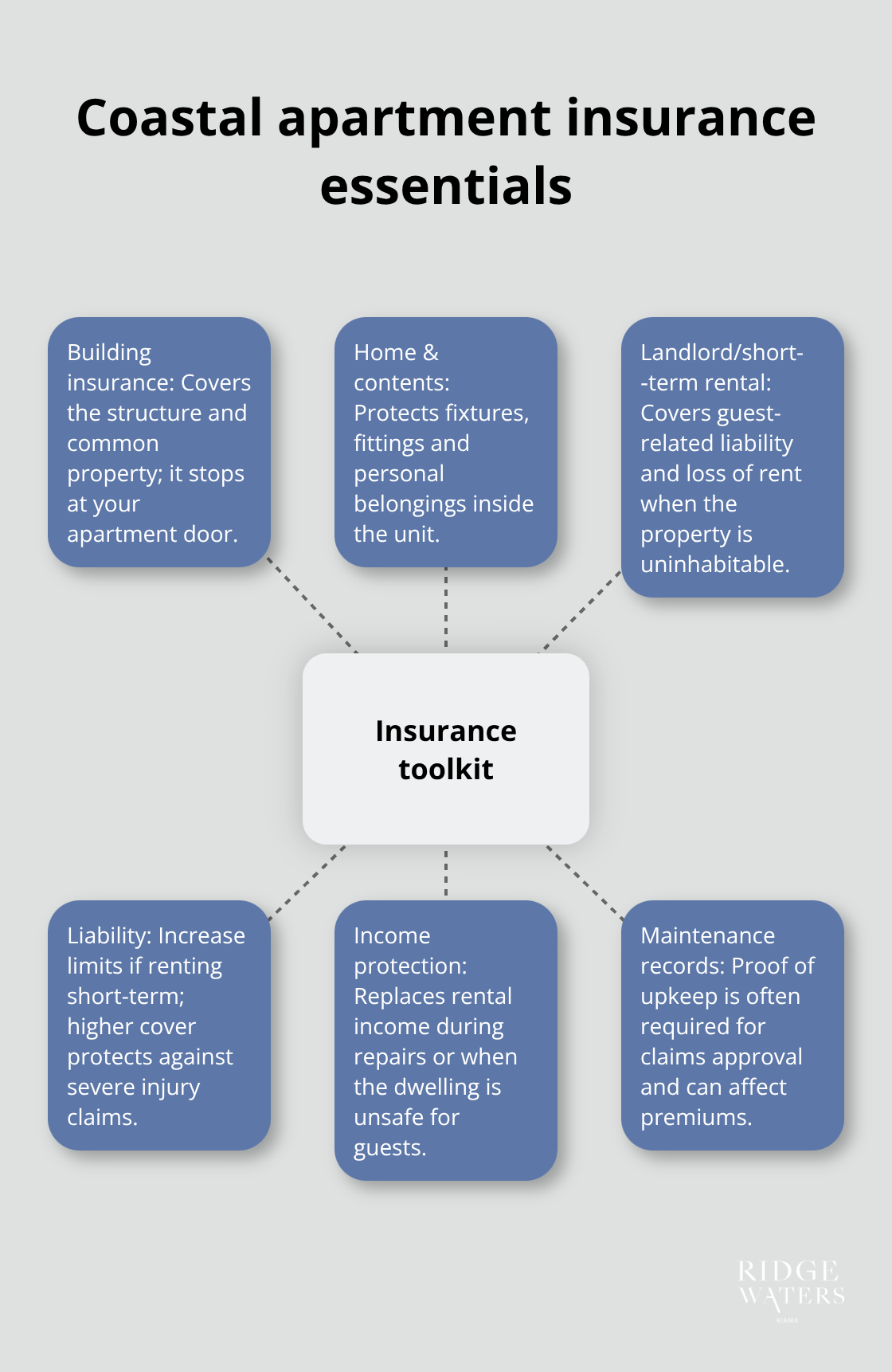

The body corporate building insurance protects the shell-fire, storm, subsidence-then stops at your apartment door. Your stuff? Your fault. Water from a burst pipe inside your unit? Your problem.

Guest slips on the balcony? Also yours. Standard home and contents insurance runs AU$800–AU$1,500 a year for a coastal apartment and covers fixtures, fittings and personal property inside the walls. The policy protects your possessions, not the building’s. Read the fine print-seriously. Most insurers expressly exclude income-producing activity. Rent on Airbnb or through a holiday manager and your standard policy can be worthless the moment you take payment-the insurer can refuse all claims. You need landlord or short-term rental insurance instead-this explicitly covers guest-related liability and loss of rental income if the apartment becomes uninhabitable. Don’t assume your current insurer will quietly switch your cover; many won’t. Call ahead and get written confirmation before you list.

Income Protection Covers Lost Rental Revenue During Repairs

A three-week repair after storm damage? That’s thousands in lost bookings if you don’t have income protection. Income protection covers lost rental revenue while the place is under repair or temporarily unavailable. At Kiama-coastal places pull heavy summer demand-this isn’t hypothetical; it’s money leaving your pocket. Coastal apartments face more weather risk, water intrusion and salt-air corrosion, which can lead to long repairs. Without income protection a single storm can erase months of profit. Coverage kicks in when damage makes the property uninhabitable or unsafe for guests. You’ll need to document repair timelines and lost bookings to claim-so keep meticulous records of your calendar and income. Most policies cover the gap between damage and when you can safely re-list.

Liability Coverage Protects You From Guest Injuries and Legal Claims

Liability is where owners get lazy-and that’s dangerous. If a guest suffers a serious injury in your unit, they can sue you personally. Typical contents policies often include only AU$5–AU$10 million in liability cover-sounds like a lot until a spinal injury lands on your doorstep. If you rent short-term, bump it to AU$20 million-the premium increase is small (usually AU$200–AU$400 a year) and the protection is huge. Legal liability for landlords also covers tenant disputes, breaches of tenancy laws and bond fights-expect AU$500–AU$1,000 annually depending on insurer. Read the PDS (product disclosure statement) closely-many policies exclude claims if you fail to maintain the property to code or if you defer repairs. Your reserve fund and a proactive maintenance schedule aren’t just good money sense-they’re policy requirements.

Maintenance Records Determine Claim Success or Denial

Coastal properties age faster, and insurers notice. A five-year-old roof membrane with early salt corrosion can trigger exclusions or premium hikes if you can’t prove you maintained it. Get a building inspection every three years and keep receipts for everything-pest control, waterproofing, balcony sealing. When you claim, the insurer will ask for proof of maintenance. Sloppy records equal denied claims. Salt spray and moisture accelerate wear on cladding, balconies, seals and fixtures-insurers expect you to address those issues proactively. Document everything: service dates, contractor names, work done, and costs. That paper trail is what protects you when your claim arrives on the insurer’s desk.

Solar Systems and Coastal-Specific Installations Need Explicit Coverage

Ask whether your insurer covers solar hot water systems and other coastal-specific installations-many policies exclude solar parts or slap on hefty surcharges. At Kiama, where sustainable systems are common, this matters-you don’t want to be surprised by a AU$3,000 repair bill you assumed was covered. Confirm coverage for any non-standard installation before purchase or upgrades. Some insurers treat solar as a separate item needing a rider; others bundle it but cap payouts. Get it in writing before you commit.

Final Thoughts

Owing at Ridgewaters Kiama – welcome to the reality show of coastal ownership. The price tag is the opening act; the real play is the ongoing cost. Body corporate fees creep up 3–5% a year, surprise repairs arrive like bad guests, and seaside exposure ages everything faster than its inland cousin. The owners who sleep at night? They planned for the whole thing.

Your financial defence? Three pillars – simple, brutal, non-negotiable. First, build reserves now. Use the 1–4% rule tied to your apartment’s age and value, then split that pot into routine maintenance, capital expenditure and emergency repairs (yes, keep them separate – commingling is how you get surprised). Second, insure properly: building insurance for the shell, home and contents for what’s inside, and rental insurance if you earn income from short-term lets – most standard policies exclude income-generating activity, so don’t assume you’re covered. Third, records – service dates, contractor names, invoices – file them like your claim depends on it because, well, it will when the insurer asks for proof.

Do the homework annually: revisit your financial plan, scan body corporate minutes for any flagged capital works, monitor that reserve balance like it’s your emergency heart rate. Coastal builds deteriorate faster – a five-year-old at Kiama will often demand planning more aggressive than an inland building twice its age. Be proactive. It’s the only thing that stops a steady bleed of deferred maintenance and the occasional, wallet-emptying surprise.