At Ridgewaters Kiama, we often get asked: “How much can an SMSF borrow to buy property?” It’s a common question for those looking to diversify their retirement savings through real estate investments.

Self-Managed Super Funds (SMSFs) offer unique opportunities for property investment, but they come with specific rules and limitations. In this post, we’ll break down the factors that determine an SMSF’s borrowing capacity and provide practical insights for potential investors.

Understanding SMSF Property Investment

What Is an SMSF?

A Self-Managed Super Fund (SMSF) is a private superannuation fund that you manage yourself. It offers more control over your retirement savings, including the ability to invest in property. This option appeals to many Australians, especially those interested in high-value areas like Kiama, where property has shown strong growth potential.

Benefits of SMSF Property Investment

Investing in property through an SMSF offers several advantages:

- Tax Benefits: Rental income is taxed at the concessional super rate of 15% (often lower than personal income tax rates).

- Capital Gains: Property investments may receive favourable tax treatment on capital gains.

- Diversification: Real estate can add diversity to your investment portfolio.

- Control: You have direct control over property selection and management.

In Kiama, where tourism thrives, SMSF investors have the option to generate income through short-term rentals and Airbnb. This flexibility can potentially boost returns, especially during peak holiday seasons.

SMSF Regulations

The Australian Taxation Office (ATO) strictly regulates SMSFs to ensure they serve their intended purpose: funding retirement. Key rules include:

- No Personal Use: You can’t live in or rent a property owned by your SMSF.

- No Related Party Rentals: Your relatives can’t rent the property either.

- Sole Purpose Test: The property must be solely for the benefit of fund members’ retirement.

Limited Recourse Borrowing Arrangements (LRBA)

SMSFs must use a specific structure called a Limited Recourse Borrowing Arrangement (LRBA) when borrowing to purchase property. This structure protects other assets in your fund if the property loan defaults.

Compliance Requirements

Compliance is a cornerstone of SMSF property investment. You must:

- Keep detailed records

- Have your fund audited annually

- Lodge tax returns

- Adhere to all ATO regulations

Non-compliance can result in significant penalties from the ATO.

Understanding these regulations is vital before investing in property through an SMSF. While the potential benefits are significant (especially in prime locations like Kiama), it’s essential to approach this investment strategy with a clear understanding of the rules and responsibilities involved.

Now that we’ve covered the basics of SMSF property investment, let’s explore the specifics of how much an SMSF can borrow for property purchases.

How Much Can Your SMSF Borrow?

Understanding Limited Recourse Borrowing Arrangements (LRBAs)

Limited Recourse Borrowing Arrangements (LRBAs) open the door to property investment through your SMSF. These structures allow your SMSF to borrow money to purchase a single asset, such as a property in Kiama. The unique feature of an LRBA protects your other SMSF assets if the loan defaults. This means the lender can only claim the property purchased with the borrowed funds, not your entire SMSF portfolio.

Borrowing Limits for SMSFs

SMSFs don’t face a set dollar limit on borrowing. Instead, the borrowing capacity depends on several factors. Most lenders cap the loan-to-value ratio (LVR) at 70-80% for SMSF property loans. This translates to a substantial deposit requirement – typically 20-30% of the property’s value.

For example, if you want to purchase a $1 million apartment in Kiama, you might need a deposit of $200,000 to $300,000. The exact amount will vary based on your lender’s policies and your SMSF’s financial position.

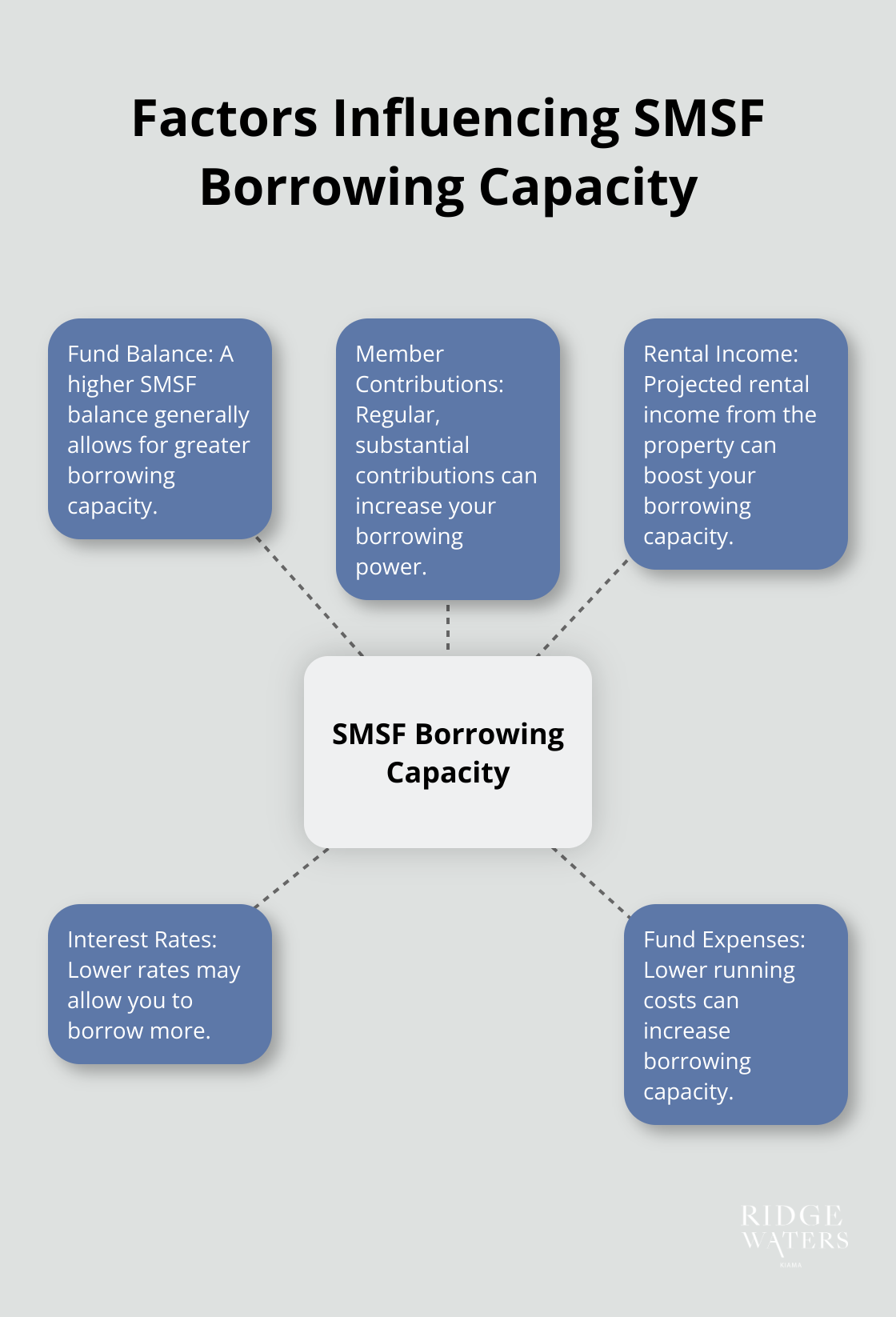

Factors Influencing Your SMSF’s Borrowing Capacity

Several elements affect how much your SMSF can borrow:

- Fund Balance: A higher SMSF balance generally allows for greater borrowing capacity.

- Member Contributions: Regular, substantial contributions can increase your borrowing power.

- Rental Income: Projected rental income from the property can boost your borrowing capacity.

- Interest Rates: Lower rates may allow you to borrow more.

- Fund Expenses: Lower running costs can increase borrowing capacity.

The Kiama Advantage

Kiama’s property market presents unique opportunities for SMSF investors. With its strong tourism sector, properties here often generate higher rental yields than in many other areas. This can positively impact your SMSF’s borrowing capacity.

For instance, a Kiama apartment used for short-term rentals might generate higher income than a long-term rental in a less popular area. This increased income potential could allow your SMSF to service a larger loan.

However, it’s important to note that while Kiama’s market is attractive, your SMSF’s primary goal must always be to provide for your retirement. Any investment decision should align with this objective and comply with all relevant regulations.

Professional Guidance

Successful SMSF property investors typically work closely with financial advisers and SMSF specialists to determine their optimal borrowing strategy. This ensures they maximise their investment potential while staying within the bounds of SMSF regulations.

Now that we’ve explored the factors affecting your SMSF’s borrowing capacity, let’s look at how to calculate this capacity more precisely.

How to Calculate Your SMSF’s Borrowing Power

Assess Your SMSF’s Financial Position

Start with an evaluation of your SMSF’s current assets and liabilities. This includes cash, shares, existing properties, and any outstanding debts. An SMSF with $500,000 in assets and no liabilities stands in a strong position to borrow.

Next, examine your fund’s cash flow. Consider member contributions, investment income, and any rental income from existing properties. A steady cash flow strengthens your borrowing capacity. For instance, an SMSF that receives $50,000 in annual contributions and $20,000 in investment income has $70,000 available to service a loan.

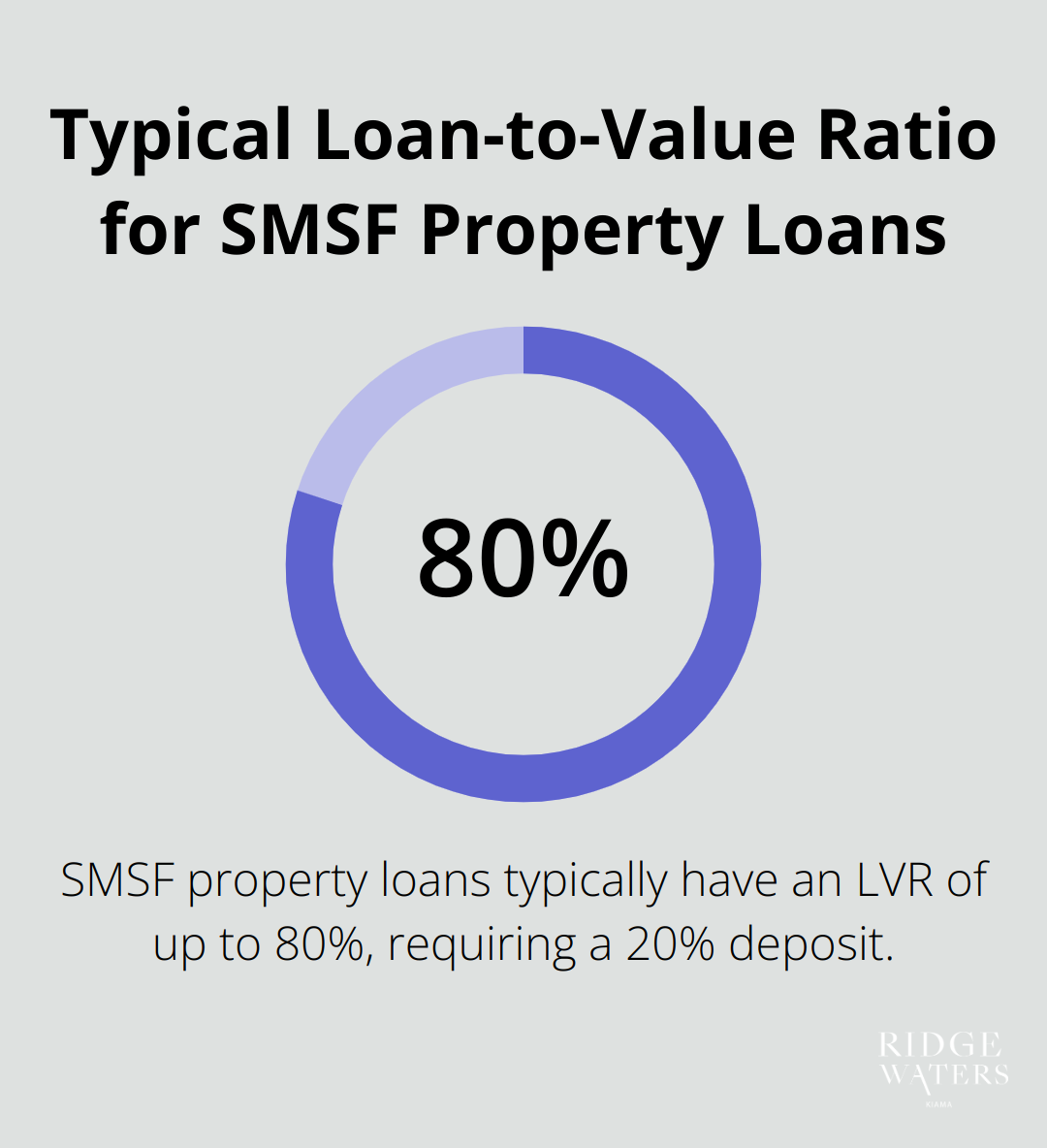

Understand Loan-to-Value Ratios

SMSF property loans typically require a loan-to-value ratio (LVR) of 80%, which means you’ll need to provide a 20% deposit of the property’s value. In Kiama’s current market, where median house prices hover around $1.2 million, you’d need a deposit of $240,000 for an average property.

Let’s break this down with a real example. If you’re considering a $900,000 apartment in Kiama, with an 80% LVR, you could potentially borrow up to $720,000, requiring a $180,000 deposit from your SMSF.

Project Income and Expenses

Lenders will scrutinise your SMSF’s ability to service the loan. They’ll look at projected rental income from the property and your fund’s other income sources. In Kiama, short-term holiday rentals can yield higher returns than long-term leases. A well-located apartment might generate $40,000 to $50,000 annually in rental income.

However, don’t overlook expenses. These include property management fees, maintenance costs, and potential vacancy periods. Try to budget for 20-30% of rental income going towards these expenses.

Your SMSF’s other ongoing costs, such as administration fees and insurance premiums, will also factor into the borrowing capacity calculation. Typically, these run Between $2,000 to $5,000 annually for a moderately sized SMSF.

Consider Kiama’s Unique Market

Kiama’s property market presents unique opportunities for SMSF investors. With its strong tourism sector, properties here often generate higher rental yields than in many other areas. This can positively impact your SMSF’s borrowing capacity.

For instance, a Kiama apartment used for short-term rentals might generate higher income than a long-term rental in a less popular area. This increased income potential could allow your SMSF to service a larger loan.

Seek Professional Guidance

Successful SMSF property investors typically work closely with financial advisers and SMSF specialists to determine their optimal borrowing strategy. This ensures they maximise their investment potential while staying within the bounds of SMSF regulations.

Final Thoughts

SMSF property investment offers a powerful strategy for retirement wealth building. The amount an SMSF can borrow to buy property depends on factors such as fund balance, cash flow, and the specific property. Thorough planning and strict adherence to regulations form the foundation of successful SMSF property investments.

Professional advice plays a vital role in navigating SMSF property investment complexities. Financial advisers and SMSF specialists help determine optimal borrowing strategies, ensure ATO compliance, and maximise investment potential. These experts provide invaluable guidance for those exploring how much their SMSF can borrow for property purchases.

Ridgewaters Kiama offers luxury apartments that could fit well in an SMSF property portfolio. With options for permanent residency and short-term rentals, our properties provide versatile investment opportunities in a prime coastal location. We encourage investors to educate themselves on SMSF regulations, seek professional guidance, and carefully consider their long-term financial goals.